Sports Betting Is Wrecking America’s Credit Scores — The Fed Just Proved It

For years, the gambling industry has maintained that legalizing sports betting brings sports wagering out of the shadows, protects consumers, and provides a massive new tax revenue stream for states. While the tax revenue part is undeniably true, a landmark new study from the New York Federal Reserve is blowing a massive hole in the “consumer protection” argument.

According to the report released in late March 2026, the rapid expansion of legal mobile sports betting is directly linked to plummeting credit health across the United States.

The data paints a grim picture: in the 30-plus states that have legalized mobile wagering since 2018, credit delinquencies have spiked, bankruptcy rates have jumped, and the average credit score has dropped. The financial carnage is most severe among young men, the exact demographic most heavily targeted by sportsbook advertising.

This is not an anti-gambling advocacy group making these claims. This is the Federal Reserve Bank of New York, using massive datasets of consumer credit reports to track exactly what happens to a state’s financial health the moment the sportsbooks go live.

The Delinquency Jump in Legal-Betting States

The NY Fed researchers analyzed credit report data before and after legalization in various states. What they found was a clear, measurable “deterioration in repayment performance” that tracked perfectly with the arrival of legal sports betting apps.

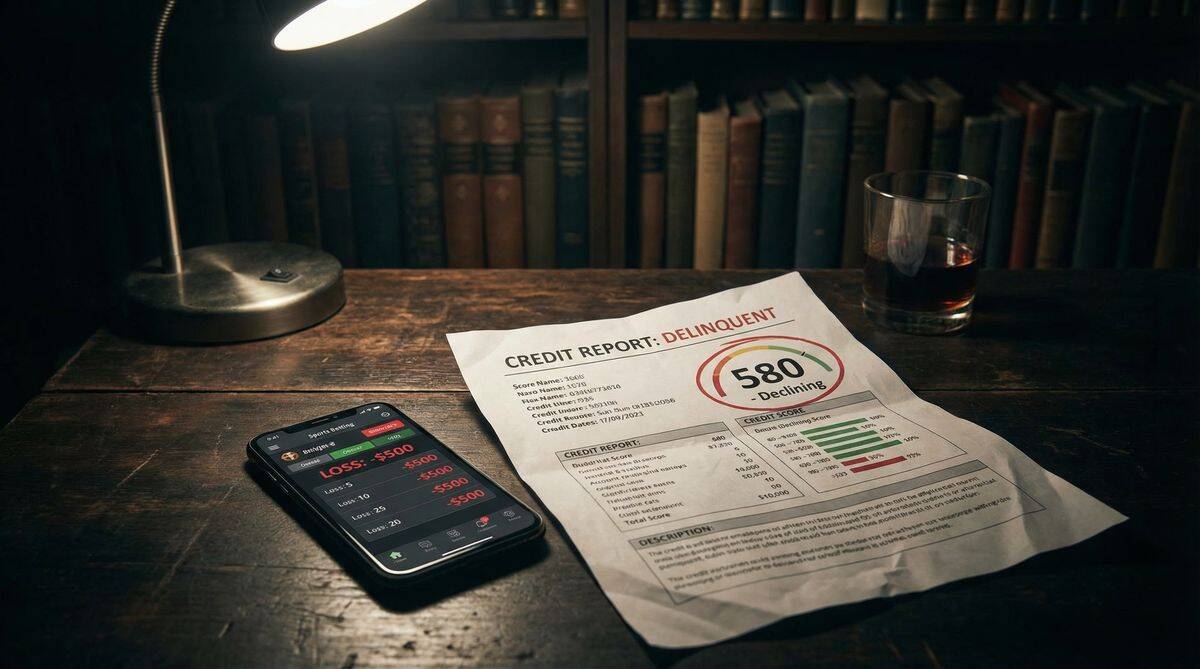

Overall, credit delinquency rates—meaning payments on credit cards or auto loans that are 90 days or more past due—rose by 0.3 percent in states where betting was legalized.

While 0.3 percent might sound small, it represents a massive number of individuals falling behind on their bills across a state’s entire population. But the real story is found when you zoom in on the actual bettors.

Inside the NY Fed paper — Staff Report 1184 by Jacob Goss and Daniel Mangrum, which ran a two-way fixed-effects comparison of “Eventually Legal” states against “Never Legal” states using the NY Fed’s Consumer Credit Panel (a 5 percent sample of anonymized Equifax credit reports) — the trajectory gets steeper the longer legalization is in place. Three years after a state goes legal, delinquency in that state’s counties climbs past half a percentage point above the pre-legalization baseline. And the effect isn’t spread evenly: among under-40 bettors living in “spillover” counties along the border of a legal state, credit-card delinquencies jumped 1.25 percentage points and auto-loan delinquencies jumped 0.78 percentage points.

“Following the legalization of sports betting in a state, credit delinquencies increase, driven by those under 40 years old,” the report stated bluntly. The researchers also noted “spillover effects” into neighboring states where betting is not yet legal, as residents simply drive across the border to place their wagers.

The Gen Z and Millennial Debt Crisis

The financial damage is not distributed equally. The NY Fed staff report, along with a separate 2025 paper by Brett Hollenbeck (UCLA Anderson), Poet Larsen, and Davide Proserpio (both at USC), highlights that younger Americans are bearing the brunt of the crisis.

The Hollenbeck paper found that, four years after a state legalized online betting, the odds of a bankruptcy filing in that state climbed 25 to 30 percent, and consumers exposed to online sports gambling saw their average credit score fall by roughly 12 points. A separate analysis by Fortune noted that credit delinquencies surged by an incredible 26 percent specifically for bettors under the age of 40.

This demographic reality aligns perfectly with the marketing strategies of the major operators. Sportsbooks have spent billions of dollars on advertising featuring celebrities, athletes, and influencers specifically designed to appeal to Gen Z and millennial men. The gamification of the apps—with constant push notifications, live in-game betting, and “risk-free” promotional offers—is built to drive engagement from a generation raised on smartphones.

Christopher Welsh, an addiction psychiatrist at the University of Maryland, told NPR that the landscape has fundamentally shifted. “It’s almost all online sports betting now,” Welsh said. He noted that he is increasingly hearing from parents who receive calls from bookies or collection agencies because their high school or college-aged children owe tens of thousands of dollars.

A “K-Shaped” Credit Economy

The NY Fed findings arrive at a time when the broader American credit landscape is already showing signs of strain. The national average FICO score has dipped to 714, down two points over the last year.

However, credit experts point out that we are experiencing a “K-shaped” credit economy. Ethan Dornhelm, head of scores analytics at FICO, recently noted that there is a record share of consumers demonstrating strong credit behaviors, pushing their scores higher. At the same time, consumers at the bottom of the K are seeing their financial health deteriorate rapidly.

Sports betting appears to be a significant downward force on that lower arm of the K. Matt Schulz, chief credit analyst at LendingTree, explained the dynamic to CNBC: “Most Americans have precious little margin for error when it comes to their finances, and while sports gambling can help in that area when you win, the truth is that it is far more likely to end up hurting more than it helps in the long run.”

This creates a dangerous cycle. A young bettor living paycheck to paycheck hits a bad streak, maxes out a credit card to chase their losses, and suddenly finds themselves 90 days delinquent. Their credit score tanks, making it harder to secure an auto loan, rent an apartment, or even pass a background check for a job.

The $167 Billion Question

The scale of the industry makes these individual financial tragedies a macroeconomic issue. In 2018, before the Supreme Court struck down the federal ban on sports betting (PASPA), Americans legally wagered roughly $7 billion on sports, almost entirely in Nevada.

By 2025, that number had exploded to $167 billion—a nearly 24-fold increase in just seven years. The American Gaming Association projected that $3.3 billion was wagered legally on the 2026 March Madness tournaments alone, a 54 percent jump over the past three years.

With over half a trillion dollars wagered since 2018, the profits for the operators are massive. But those profits are heavily concentrated. A 2024 Wall Street Journal investigation found that 70 percent of the profits from one major online gambling company came from less than 1 percent of its users.

The industry relies on a small percentage of high-volume bettors to generate the vast majority of its revenue. The NY Fed data strongly suggests that a significant portion of that revenue is being funded by credit card debt and missed loan payments.

What Happens Next?

The gambling industry has historically relied on the argument that adults should be free to spend their entertainment budget however they choose. Ted Rossman, a senior industry analyst at Bankrate, summarized this view: “It’s okay to spend money on the occasional indulgence… you just need to budget for it.”

But the research challenges the idea that sports betting is just harmless entertainment. When one industry drives a measurable rise in credit delinquencies across legal-betting states and a 25-30 percent increase in bankruptcy filings in states with online betting, it stops being a personal budgeting issue and becomes a public policy crisis.

As the data continues to mount, pressure will inevitably build on state regulators and federal lawmakers to intervene. We are already seeing pushback, from proposed bans on college prop bets to discussions of federal excise taxes on gambling revenue.

The “Wild West” era of mobile sports betting expansion is likely coming to a close. The NY Fed has provided the receipts, and the bill is coming due.

If you are looking to better understand how sportsbooks operate and how to manage your bankroll responsibly, you can read our guide on best sports betting apps.

If you or someone you know is struggling with sports betting debt or gambling addiction, please visit our responsible gambling resources for immediate help and support.

Did the Federal Reserve really study sports betting?

Yes. In March 2026, researchers at the Federal Reserve Bank of New York published a staff report analyzing consumer credit data in states before and after the legalization of mobile sports betting.

How does sports betting affect credit scores?

The NY Fed staff report found that in states that legalized sports betting, credit delinquencies (payments 90+ days late) rose about 0.3 percentage points state-wide, climbing past half a percentage point above baseline three years after legalization. A separate 2025 paper by Hollenbeck, Larsen, and Proserpio (UCLA Anderson and USC) found that bankruptcy odds increased 25 to 30 percent four years after a state legalized online sports betting.

Who is most financially affected by sports betting?

The data shows that young men under the age of 40 are experiencing the sharpest drop in credit health and the highest surge in credit delinquencies following legalization.

Can I use a credit card to bet on sports?

While some states and sportsbooks allow credit card deposits, it is highly discouraged. Credit card companies often treat gambling deposits as “cash advances,” charging immediate, exorbitant fees and high interest rates. You can learn more in our guide to online gambling banking options.

What is the “K-shaped” credit economy?

It refers to a growing divide where financially secure consumers are improving their credit scores (the upward arm of the K), while financially vulnerable consumers are taking on more debt and seeing their scores drop (the downward arm).